Panic Selling: Where the Weak Lose and the Wise Win

March 10, 2026

Introduction: Panic is not a strategy. It is surrender.

We see it repeatedly. A note of caution appears, and some investors immediately assume catastrophe. Positions get dumped into weakness, often near the worst possible moment. Fear turns a temporary pullback into a personal crisis. Losses get locked in while someone calmer quietly takes the other side.

That reaction misses the point entirely. We do not panic. When gains become sizable, we bank them, but exits driven by fear rarely end well. Panic selling usually transfers assets from impatient hands to patient ones. Markets reward those who stay composed while others react emotionally.

During our August 2021 update, we warned that a correction would shake out weak hands. That process was never meant to signal collapse. Pullbacks often reflect emotional overreaction rather than structural damage. They cleanse excess optimism and reset the field for the next advance.

Moments like these are useful training grounds. Investors should record how they react when markets turn volatile. A trading journal reveals patterns most people never notice. Over time, the real opponent becomes clear. It is rarely the market. It is the investor’s own impulses.

Fear presents itself as protection. In reality, it often pushes investors to abandon sound positions simply because the tape turns ugly. The patient investor studies those moments carefully. When emotion dominates the crowd, value frequently appears where others see danger.

Every panic creates two groups. One sells in distress. The other waits, or quietly accumulates. The difference rarely lies in information. It lies in discipline.

Panic Selling: Where the Weak Lose and the Wise Win

Panic selling and crashes are not the same event. A crash is a market condition. Panic is a human reaction to it. The two often arrive together, but they are not identical.

History shows that extreme selloffs often become the soil from which major opportunities grow. The 1929–1932 collapse destroyed confidence, yet long-term investors who entered near the depths eventually saw enormous gains as the economy rebuilt. The 1987 crash erased roughly a quarter of market value in a single day. Within a few years, the market recovered and moved to new highs.

The pattern repeated during the dot-com collapse. Investors who chased technology stocks during the mania were crushed. Those who waited until the fear phase, when valuations reset and speculation drained out, found strong opportunities in the survivors of that wreckage.

The same dynamic appeared during the 2008 financial crisis. Panic ruled the headlines. Yet that collapse also produced some of the most attractive entry points of the past generation.

The key distinction lies in timing and psychology. Opportunity rarely appears at the first sign of a decline. It usually emerges later, when fear peaks and forced selling distorts prices. Markets need time to flush excess optimism before value reappears.

Every crash, therefore, carries two possibilities. It can destroy investors who react emotionally, or it can reward those who remain patient and wait for conditions to stabilise.

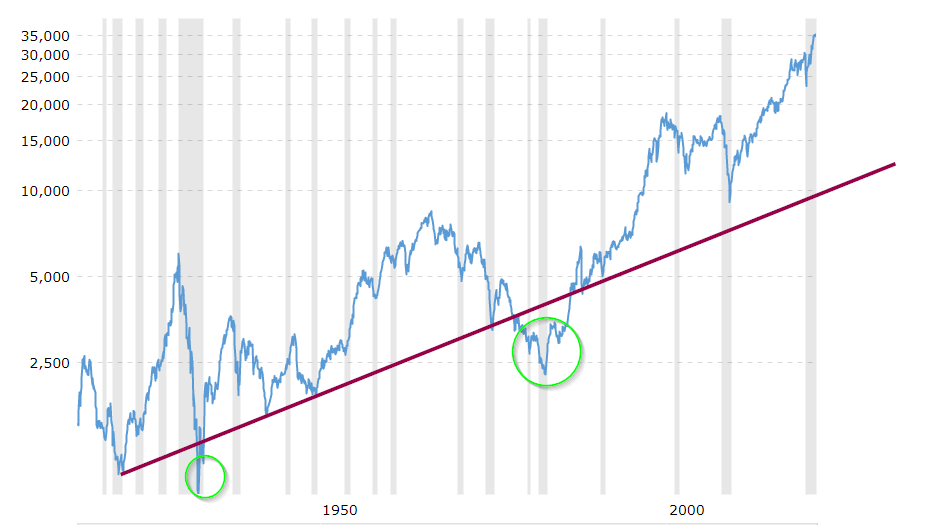

No investor has ever proved that surrendering to panic creates long-term success: look at the chart below as an example. Fear feels protective in the moment, but over decades, it has consistently transferred assets from the anxious to the disciplined.

Euphoria works in the opposite direction. When everyone believes the market can only rise, risk quietly accumulates beneath the surface. Those moments often precede the most damaging declines.

Markets move through these emotional extremes again and again. Fear creates opportunity. Euphoria creates vulnerability. The investor’s task is not to eliminate emotion, but to recognise where the crowd stands within that cycle.

Why Most Investors Fail

Most investors fail for a simple reason. They react instead of acting with a plan. They chase excitement when prices surge and abandon positions when markets turn hostile. Emotion drives the decision, not structure.

That dynamic destroys discipline. Systems require patience and sequencing. Panic demands immediate relief. The investor who yields to that pressure usually exits near exhaustion points where opportunity quietly begins forming.

Our approach inverts that behaviour. We lean into volatility when others search for comfort. We reduce exposure when enthusiasm becomes universal. Markets tend to reward the investor willing to stand still while the crowd swings between euphoria and despair.

H.L. Mencken captured the mechanism in a different context when he observed that leaders keep the public alarmed with an endless series of threats. Replace politics with markets, and the pattern becomes familiar. Financial media thrives on urgency. Fear keeps the audience engaged. The herd reacts, while patient capital quietly accumulates value created by that fear.

Strategic Discipline

Our framework rests on three simple principles.

First, capital is deployed gradually. Exposure begins small, then increases as conditions confirm the thesis. This layered approach reduces risk while preserving flexibility. Markets reward patience far more often than aggression.

Second, progress must remain deliberate. Emotional trading invites costly mistakes because urgency replaces judgment. Calm execution preserves both capital and perspective.

Third, investing should not feel like chaos. Constant anxiety usually signals that the investor is reacting to noise instead of structure. Price behaviour, sentiment extremes, and liquidity flows offer far more useful signals than the daily flood of commentary.

Volatility and Opportunity

Market turbulence often signals transition rather than destruction. When liquidity expands, rebounds can unfold with surprising speed. The recovery following the COVID shock illustrated that reality clearly. Panic dominated the headlines, yet the rebound arrived far sooner than most observers expected.

Crashes themselves follow a recognisable sequence. Tension builds quietly, uncertainty spreads, and fear eventually forces weaker participants to sell. Once the selling pressure exhausts itself, stronger hands accumulate positions at far more attractive valuations. Recovery then begins while pessimism still dominates the narrative.

This process has repeated for generations. Volatility transfers assets from impatient holders to disciplined ones. Large institutions require liquidity to build positions, and periods of fear often provide that supply.

The lesson is straightforward. Panic and euphoria represent opposite distortions within the same cycle. Investors who recognise those emotional extremes gain a structural advantage. Those who react to them usually become part of the transfer.

Understanding that difference does not eliminate risk. It simply clarifies where opportunity tends to appear.